Shaft design at Anglo American’s Woodsmith underground polyhalite mine in the UK includes a fore shaft, shown here during construction, that is 33 m (108 ft) in diameter. The mine’s production and service shafts below the fore shaft are 7.5 m in diameter and will be sunk to 1,600 m (5,250 ft). The company said it increased each shaft’s diameter by 10% over the original design in order to eliminate bottlenecks and maximize production and ventilation. (Photo: Anglo American)

The fertilizer mineral market has lately resembled a rollercoaster ride, but the soft rock sector’s project pipeline holds a steady flow of investments ranging from millions to billions

By Russell A. Carter, Contributing Editor

The relative strength of an industrial sector can be at least partially judged by the characteristics of its most notable projects; for instance, their announced production capacity, level of technological sophistication and capital cost. Applying these measures to soft rock mining yields results that compare favorably with many of the generally more-publicized top projects in various hard rock mining segments, with some soft rock projects featuring capital costs in the multi-billion dollar range, advanced technologies and heightened environmental impact sensitivity.

With market concerns focused on availability and prices of critical mineral commodities such as copper, lithium, nickel, cobalt and rare earth elements, it’s easy to overlook the importance of the common soft rock minerals – potash, phosphate, salt, graphite and even gypsum – in the world economic picture. However, potash, for example, is already considered a critical mineral in Canada, and in the United States some legislators are pushing for inclusion of both potash and phosphate on the U.S. critical minerals list as a step towards strengthening the nation’s food security level.

Additionally, companion bills were introduced earlier this year in the U.S. House of Representatives and Senate aimed at speeding up the expensive and lengthy permitting process for both hard- and soft-rock mines in the USA, as part of a larger attempt to expedite oil and gas, coal and battery-metal development. As the Fertilizer Institute, the U.S. industry’s potash/phosphate lobbying organization, pointed out recently in support of the proposed legislation, typical delays arising from the existing process include an effort to obtain a permit to mine phosphate in Florida that took nearly 10 years and tens of millions of dollars in expert fees, studies, legal analysis, and legal fees; or an expansion permit for an existing mine that has been in limbo for over 12 years at a cost of over $25 million and has yet to be approved. Citing threats posed by the bill to public health and environment, H.R. 1 was strongly opposed by the Biden Administration, but was approved by the House in March.

Adjusting to the Market

Fertilizer is a globally traded commodity subject to international pressures and geopolitical events, and potash production, a major source of the potassium included in most fertilizers, is not immune from volatile market movements. Until 2021, according to S&P Global Commodity Insights, increased capacity and an expansion of the potash supplier base heightened price competition and ensured a buyers’ market for Muriate of Potash or MOP, the most widely used potash fertilizer product. However, high demand and uncertainty over supply in 2021 reversed all previous price reductions, with market prices more than doubling.

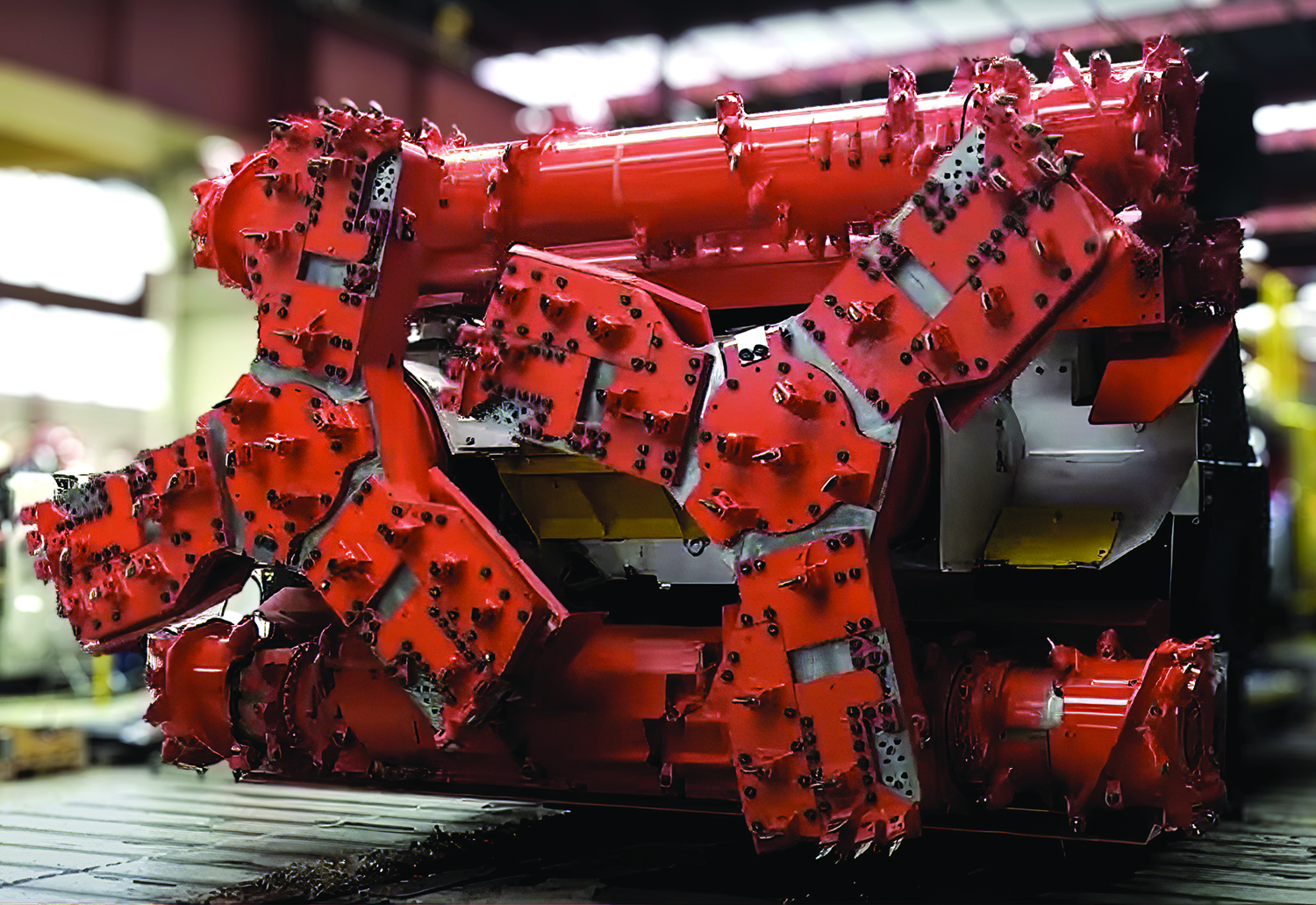

BHP’s Jansen potash operation will employ Sandvik MF460 borer mining machines that feature a variable-height cutting head that can cut a much larger swath per pass than the conventional borer machines commonly in use throughout the potash mines of Saskatchewan. Four mining systems, comprising an MF460 paired with Sandvik’s PO140 Extendable Belt System, are expected to produce roughly 2.7 million mt/y each at Jansen. (Photo: BHP)

The market has since cooled; prices dropped and some large producers readjusted their outlook. Nutrien, the company formerly known as Potash Corp. of Saskatchewan, announced in August that it was pausing its potash production ramp-up plans indefinitely and reducing its planned capital spending by $200 million. Mosaic Co., another major producer, temporarily curtailed potash production late in 2022 at its Colonsay, Saskatchewan, mine in Canada, citing lower-than-expected usage. However, the company restarted the mine in the third quarter of 2023 due to strengthening North American demand.

Despite the recent fertilizer market disruptions, a number of major soft-rock mine development efforts are in the works. Here’s a quick sample of current projects under way:

• Switzerland-based EuroChem Group continues to ramp up production at its Verkhnekamskoe potash deposit near Perm, Russia, considered one of the largest in the world. Within this deposit, EuroChem Usolskiy has secured rights to over 2.3 billion metric tons (mt) of reserves with an average KCI content of 30.8%, underpinning a predicted active mine life of 35-plus years.

With a mine and processing plant built and entering operations, the facility is currently producing potash at a rate of 1.1 million mt/y, and is on the way to its full first-phase ramped-up capacity of 3 million mt/y from a two-shaft, four production-train operation. The second phase comprises the construction of a third shaft, which has already begun, and an expanded processing plant, which will increase ore mining capacity by nearly 50% to 14.4 million mt, lifting final production capacity to 4 million mt/y.

• EuroChem also completed the acquisition of the Serra do Salitre phosphate project in Brazil in February 2022, taking over the advanced-stage mine and plant in Minas Gerais state. The complex comprises an open-pit phosphate mine with over 350 million metric tons of reserves and a plant with production capacity of 1 million mt of fertilizer per year. The deal was valued at $452 million, and EuroChem said it will invest a similar amount to fully implement the project. Fertilizer production is expected to launch in 2024 and reach full capacity in 2025. The mine and processing plant are currently in operation and produce about 500,000 mt/y of phosphate rock.

• Emmerson, an Isle of Man-based company whose primary focus is on developing the Khemisset potash project located in Northern Morocco, pointed to a recently completed feasibility study completed by Golder Associates that it said confirmed the findings from a scoping study, which showed that Khemisset has the potential to be a world class, low capital cost, high margin potash mine. The study, according to the company, said Khemisset could produce approximately 810,000 mt/y of K60 MOP during steady state operations over the initial 19-year mine life. In addition, the project comes with a low pre-production capital cost of $387 million, less than half of its global peer average capital intensity.

• Asia-Potash International is advancing a project in Khammuan province, central Laos, where it currently holds 214.8 km2 meters of potash mining rights and 48.5 km2 of potash prospecting rights, which the company said could be converted to 1 billion mt of pure potassium chloride resources, making it the largest in Asia in terms of potash resource count. The project is targeted to reach a production capacity of 5 million mt/y by 2025 then expand to 7-10 million mt/y in the future depending on market demand.

• In September, Reuters reported that authorities from Argentina’s Mendoza province had finalized the selection process for a $1 billion investor to help develop the Rio Colorado potash project, more than a decade after Brazil’s Vale SA abandoned its efforts there due to price pressures. Completion of the partially constructed complex has been estimated to take five years with a potential annual production of 1.5 million mt. Before it shelved the project, Vale reportedly spent $2.2 billion to partially build a mine, a new railway and a loading terminal. News reports indicate that current Interest from potential investors ranges from a 200,000 mt/y to a 1.5 million mt/y operation, with investment estimated at approximately $1,000 per mt.

Megaprojects Are Moving Ahead

Two large soft-rock mineral projects warrant special mention for their ranking in the multi-billion range of capital costs and for innovative design elements.

BHP said it plans to spend almost $5 billion to start development on the second phase of its Jansen potash project in Saskatchewan, and is touting the technological features of the new mine. The company recently approved an investment of $4.9 billion for stage two; this follows approval of $5.7 billion for stage one in August 2021 and a pre-stage one investment of $4.5 billion.

BHP Chief Executive Officer Mike Henry said the additional investment will transform Jansen into one of the world’s largest potash mines, doubling production capacity to approximately 8.5 million mt/y.

According to the company, the first stage is 32% complete and progressing on schedule. First production is anticipated in late CY2026. Stage two construction is anticipated to take approximately six years, and is expected to deliver first production in FY2029, followed by a ramp up period of three years.

The second stage is intended to deliver approximately 4.36 million mt/y of production at a capital intensity of approximately $1,050/mt, lower than the first stage due to the leveraging of existing and planned infrastructure. The additional $4.9 billion for stage two will be used for the development of additional mining districts, completion of the second shaft hoist infrastructure to handle higher mining volumes, expansion of processing facilities and the addition of more rail cars.

Westshore Terminals, in Delta, British Columbia, remains BHP’s main port facility to ship potash from Jansen to customers. The Jansen stage two investment includes funding to increase storage facilities at the port. BHP said it would not be initiating a formal capacity extension for the Westshore port terminal at this time and will evaluate closer to stage two reaching first production.

The visual impact of Anglo American’s Woodsmith project will be minimized by placement of much of the mine’s surface steelwork below the surface, enclosing the remaining above-ground structures in agricultural-style buildings, and surrounding the entire facility with landscaped berms. (Photo: Anglo American)

Transitioning to stage two during the construction period of stage one is expected to bring a number of operational benefits, including leveraging the experience of the integrated Jansen project team, continued use of existing contractors, reduced overheads and savings on mobilization and demobilization costs. BHP said potential synergies of $300 million have been embedded into stage two’s economics.

Longer term, Jansen has the potential for two additional expansions to reach an ultimate production capacity of 16 to 17 million mt/y, subject to studies and approvals. According to the company, Jansen has been designed with a focus on social value and sustainability and is expected to have approximately 50% less operational (Scopes 1 and 2) greenhouse gas emissions per ton of product and use up to 60% less fresh water when compared to the average potash mine in Saskatchewan.

Laura Tyler, BHP’s chief technical officer, outlined some of the reasons for the company’s robust investment commitment to the project in a presentation last December at the Melbourne (Australia) Mining Club: “Jansen will be the most advanced and sustainable potash mine ever built. As a new operation, we do not have to retrofit technology and we can install at design. It will be difficult, if not impossible, for existing potash miners to retrofit and recreate the operational advantages that we are seeking to capture over the next couple of years.

“For example, during design we wanted to provide a proven alternative to the conventional active borer technology, so we partnered with Sandvik to look at the options.” This resulted in development of Sandvik’s MF460 Borer Miner – a design upgrade of the existing MF420 machines, a number of which have been used at nearby mines. The MF series of borer miners, said Sandvik, were developed from the Marietta Miner machines built originally for the U.S. coal industry, with subsequent versions finding usage in the Saskatchewan potash mines and U.S. trona operations, dating back to the 1980s. Sandvik acquired the rights to the Marietta Miner design from National Mine Service. The MF 460s will be coupled with Sandvik’s PO140 Extendable Belt System.

She continued: “We will introduce a high degree of automation, integrated design and eventually a remote operation center like we see at WAIO, BMA and Escondida to drive the borers of the future. We will be connected to it from surface, potentially even from Saskatoon.

“Jansen Stage 1 will have just four mining systems, capable of producing the equivalent of 10 to 14 typical systems, able to monitor the ground ahead and adjust

its mining height to match the ore body. This is a sustainable advantage, with around 60% less fleet creating around a 10% operating cost saving as well as fewer active mine faces, so therefore increasing stability, and a smaller environmental footprint. Jansen, we believe, will set a new benchmark for equipment and decision automation in the potash industry.

“We will have three times the number of process sensors and 10 times the number of machine health monitoring sensors compared to the next largest producer in Saskatchewan. This, married together with the latest processing technology, means we expect to achieve an industry-leading recovery rate of around 92%, and Jansen stage one will have approximately 50% less carbon emissions per ton than the average in the basin and approximately 60% less fresh water consumed on the same basis.”

At an earlier briefing, Mike Elliot, Jansen’s former project director and now head of mining delivery, offered some insight into the mine’s shaft design and construction, noting that “shaft sinking is the most challenging part of building a potash mine in Saskatchewan, because it involves excavation and lining through several water-bearing formations. Our shafts are constructed to be completely dry by using a composite hydrostatic liner from the surface to beneath the lowest water-bearing formation.

“Most other Saskatchewan mines have opted for less capital-intensive construction by only constructing hydrostatic liners through the major water bearing formations, and as a result they experience residual seepage. This is an important differentiator because dry shafts last longer, are cheaper to maintain and deliver higher annual hoist run-times.”

Elliot said Jansen’s two shafts, each 7.3 m in diameter, are also the largest in Saskatchewan, compared with the next largest shaft in the province at around 6 m, and the average in the province of 5 m. “Our investment in a larger diameter allows us to deliver stage one production through only a single service shaft, thereby reducing upfront capital. And then for future stages, our larger diameter allows us to have four skips in our production shaft versus the typical two, and increased ventilation to support a larger mine footprint, thereby giving us the potential to achieve 16-17 million mt/y of production from Jansen alone.

“Our peers’ production is constrained at their mines due in part to smaller shaft diameters that limit both ventilation and hoisting capacity, and they will have to continue operating multiple mines to achieve the same output as Jansen,” according to Elliot.

Meanwhile, after buying the former Sirius Minerals-owned Woodsmith polyhalite property in northeastern England, Anglo American has embarked on a project development plan that could ultimately cost as much as $9 billion. The project involves sinking two 1-mile-deep shafts at the Woodsmith site and driving a 23-mile (37-km) transportation tunnel to a processing facility and port. Much of the typical above-ground infrastructure at Woodsmith will be built below surface, complemented with landscaping to minimize the visual impact on the surrounding countryside.

The company will mine a large deposit of polyhalite, perform minimal processing on the sulfate mineral and sell it as a natural, environmentally friendly fertilizer. Polyhalite previously has only been produced in small quantities and its market is not commercially proven at scale, but Anglo American said polyhalite has the potential to improve crop yields by 3% to 5%.

The company estimated it would spend around $1 billion a year to bring the project to production by 2027. It bought Woodsmith for GBP405 405 million

($488 million) in 2020 and said it has spent $1.35 billion so far expanding it. Anglo now expects production to reach about 5 million mt/y by 2030, compared with the former owner’s production estimate of 10 million mt/y in the first phase.

Anglo American recently announced a $1.7-billion write-down on the project and also set a later-than-expected start date for operations to begin. Chief Executive Duncan Wanblad gave reassurances that the write-down was only necessary because the project’s timeline had been extended, along with its budget, and that the company is intent upon setting up Woodsmith to “generate significant cashflows for many, many decades.”

The two (service and production) new shafts’ headframes are hidden in a 43-m-deep foreshaft enclosed in a standard agricultural-type building. With the project surrounded by earthwork berms, once completed most people driving past the site will be unaware of the facility, according to Anglo. The production shaft will hoist polyhalite ore to the Mineral Transport System level at –360 m, where it will be transferred to a 37-km-long conveyor system and sent to Teesside.

During a recent investor tour, Tom McCulley, CEO of Anglo American’s Crop Nutrients business, explained why the company is so confident in the project’s future and provided an update on current development status.

“First, we have the scale; we have a thick orebody seam compared to our competitors. Our seam is four to five times thicker than a typical MOP mine, which just gives us an inherent advantage over other mines and allows for efficient bulk mining within the seam.

“Second, we have a 1:1 ore to product ratio due to the geologic nature of our orebody. This is also a significant reason we will have a low SIB (stay-in-business) capex profile for the LOA (Life of Asset), there will be no waste and no development capex.

“Third, a major structural advantage for us is that we control the logistics line from pit to port and we are very close to the port – only 37 kilometers. When you compare this to other bulk fertilizer mines who must transport product on rail lines or roads across thousands of kilometers, you can appreciate just how much of a cost and structural advantage this is.

“In addition,” he explained, “we have absolutely no chemical processing and we don’t have waste, so we don’t need a tailings facility. There is minimal water used because there is very little processing needed. This product is as close you can get to applying the product right from the mine to the farm.”

McCulley then listed some key project milestones: “We expect the service shaft to reach first product in 2027, with the main driver to the shaft sinking schedule being how we progress through the Sherwood sandstone strata. The production shaft started about six months after the service shaft and therefore will be at ore level about six months after the service shaft. Once the service shaft is at depth, we will start the excavation in polyhalite to connect the two shafts and continue with the mine development.

“The two shafts will be sunk to the final elevation by Redpath using SBRs (shaft boring roadheaders). When done, these are expected to be the deepest shafts in Europe. From a status standpoint and where we sit today, the service shaft is currently at 550 meters and making good progress since starting. The production shaft started around April 2023 and is currently at 340 meters and [we are benefitting from] many of the lessons from the service shaft.”

He said the company is “making excellent progress on the tunnel excavation. Our next milestone for the tunnel will be when we pass 25.8 kilometers, this will set a world record for the longest single TBM tunnel. Beyond this we will pass our next intermediate shaft at Ladycross, where we will take a three-to four-month maintenance pause as we set up the TBM for the final push to 37 kilometers, and we expect to reach the Woodsmith mine in late 2026.

“We have a Tier 1 resource and a quality orebody which allows for efficient bulk mining methods, using room and pillar mining with continuous miners, which is a low cost, efficient and proven approach for this type of mine. We are in the process now of optimizing the mine plan to match the ramp-up plans and to ensure we set up the mine for long term success at a low cost. After we complete our optimized mine plan, we will then review short and long term technologies to ensure we have a mine that will be the benchmark for the industry for years to come,” he concluded.