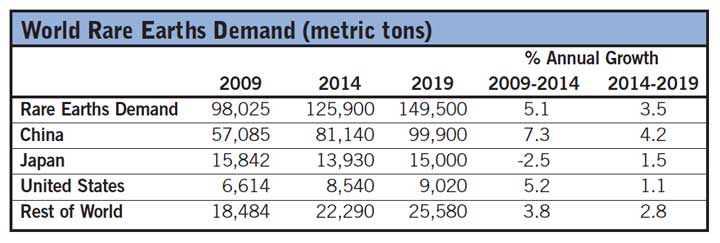

Global demand for rare earths is forecast to increase 3.5% per year to 149,500 metric tons (mt) in 2019, valued at $4.5 billion. The largest increases are forecast for the permanent magnet segment, boosted by expanding production of advanced neodymium magnets for applications such as wind turbines and hybrid and electric vehicles (H/EVs). Rising output of nickel-metal hydride (Ni-MH) batteries is also expected to fuel rare earths demand. In addition, upgrades to oil refining sectors in emerging countries are projected to boost global catalytic cracking capacity, supporting the production of fluid cracking catalysts, and associated demand for lanthanum and cerium. Rising production of steel, motor vehicles, and electronics is also expected to drive rare earths consumption. These and other trends are presented in World Rare Earths, a new study from the Freedonia Group Inc., a Cleveland-based industry research firm.

China will remain the leading consumer of rare earths, accounting for more than two-thirds of global demand in 2019. Analyst Carolyn Zulandt noted that “growth in the Chinese market will be driven by healthy increases in the country’s output of neodymium magnets, Ni-MH batteries and refinery products.”

Japan will remain the second-largest global market, benefiting from a large domestic electronics manufacturing sector and robust demand for rare earths in the production of batteries, magnets, and polishing powders. The fastest gains of any major market worldwide are projected for India, where rising domestic production of motor vehicles and metal alloys, as well as expanding catalytic cracking capacity, are expected to boost rare earths consumption. India is also developing local production of rare earth magnets, although this market will remain small in the near term.

China will continue to account for the majority of rare earths mining output through 2019, although its share of total production is expected to drop as a number of new projects in Canada, Tanzania, South Africa and other countries begin commercial production. Major output increases are also expected in Australia as Lynas continues to ramp up production following capacity expansions. However, junior mining companies looking to develop new deposits will struggle to obtain investment for these ventures as prices for rare earths will remain depressed, due in part to rampant illegal mining activities that continue to plague China’s industry.

World Rare Earths (published November 2015, 318 pages) is available for $6,300 at www.freedoniagroup.com.