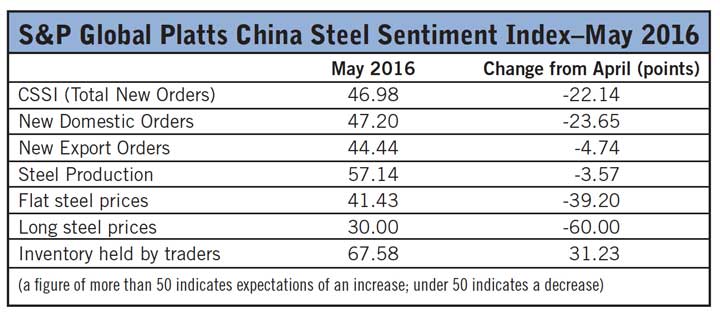

A majority of Chinese steel market participants believe prices will likely fall due to weaker domestic demand, with the outlook for construction steel particularly bleak, according to the latest S&P Global Platts China Steel Sentiment Index (CSSI), which showed a headline reading of 46.98 out of a possible 100 points in May.

The May index dropped 22.14 points from 69.12 in April, recording the weakest reading since February—and is now 42.44 points below March’s record of 89.42. A reading above 50 indicates expectations of an increase/expansion and a reading below 50 indicates a decrease/contraction.

The outlook for new domestic orders for steel for the coming month fell by 23.65 points from the previous month to 47.20 in May, while expectations for export orders edged down by 4.74 points to 44.44.

The outlook for new domestic orders for steel for the coming month fell by 23.65 points from the previous month to 47.20 in May, while expectations for export orders edged down by 4.74 points to 44.44.

Price expectations for long steel products, such as rebar, slumped by 60 points from April to 30 in May. The price outlook for flat steel products, such as hot rolled coil, fell 39.20 points to 41.43 in May. Editor’s note: the price for iron ore has dropped from $65.85 per dry metric ton (dmt) this time last month to $49.90/dmt this month.

The outlook for crude steel production in May dropped 3.57 points from the prior month to 57.14. Steel market participants expected steel inventories to start climbing again this month, with the reading for this measure rising 31.23 points from April to 67.58 in May.

“The big downturn in the outlook for domestic steel orders and prices is the big concern and unfortunately all the ingredients for a price correction appear to be in place, judging by the results of the index,” said Paul Bartholomew, senior managing editor of steel and raw materials for S&P Global Platts.

“The big and sudden shift from optimism to pessimism—particularly in the outlook for construction steel prices—is further indication of how sentiment driven the market has become,” Bartholomew said.

“Restocking has been a major reason why prices have climbed this year but steel inventories are tipped to rise while steel production is predicted to stay at current high levels. This could put prices under pressure in the next month or so,” he added.

The CSSI is based on a survey of approximately 70 to 85 China-based market participants including traders and steel mills. Data is compiled by S&P Global Platts’ Shanghai steel team.

Separate to the CSSI, the Platts China export hot rolled coil price assessment in April averaged $430/mt free on board (FOB) China. This was up 2% on $421.6/mt FOB in March.

The S&P Global Platts China Steel Sentiment Index survey plays no role in Platts’ formal price assessment processes.

For more information, visit Platts.